Total Visitors

Total Visitors  Online Users

Online Users  Today

Today  Yesterday

Yesterday

In a Nutshell

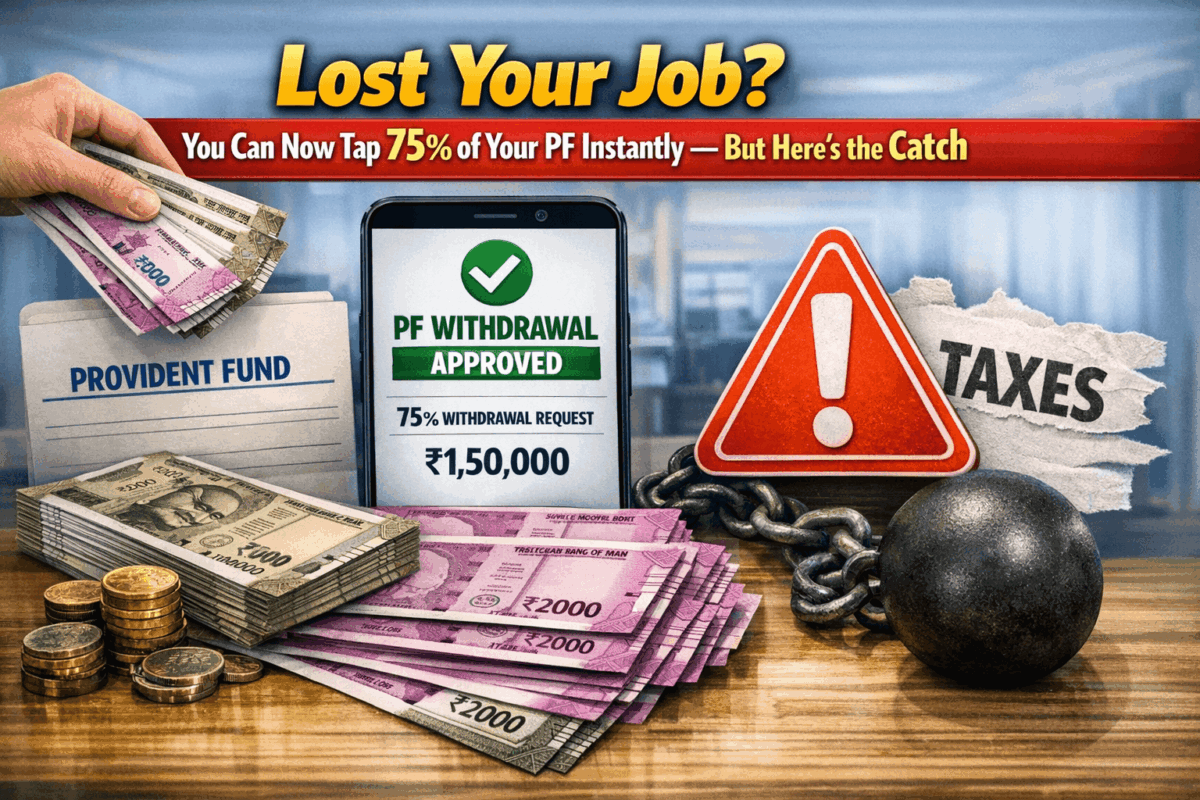

Losing a job hits your finances hard. Fortunately, the government has simplified EPF withdrawal rules so you can access 75 percent of your provident fund balance immediately after becoming unemployed. The remaining quarter stays locked for 12 months not to punish you, but to preserve a safety net for the long run.

The Breakdown

Three simple categories replace 13 confusing ones

The old EPF withdrawal system had 13 different categories each with its own documentation and approval maze. EPFO has now consolidated everything into three broad groups:

| Category | What It Covers |

| Essential Needs | Medical emergencies, education, marriage, loan repayment |

| Housing Needs | Home purchase, construction, or renovation |

| Special Circumstances | Job loss, permanent disability, migration abroad |

Unemployment falls under the “Special Circumstances” category.

The 75% now, 25% later rule and why it exists

If you are laid off or leave a job without another offer in hand:

- Immediate access: You can withdraw 75% of your total EPF balance right away no waiting period, no questions asked.

- The remainder: The remaining 25% becomes available after 12 months of continued unemployment.

Why lock 25%? EPFO explains that workers with lower salaries often withdrew their entire corpus repeatedly, never letting the magic of 8.25% annual compounding work for them. By preserving a quarter of the balance for at least a year, the scheme forces you to keep some retirement savings growing, a forced financial buffer against old-age poverty.

Big change: Employer share is now fully withdrawable

Earlier, full withdrawal of the employer’s contribution was restricted to very specific conditions like retirement or permanent disability. Under the revised framework, when you withdraw due to unemployment, both employee and employer contributions along with accumulated interest are included in the eligible amount. This significantly increases the corpus available to you during a financial crisis.

Interest rate holds at 8.25% for 2025–26

The Central Board of Trustees (CBT) EPFO’s highest decision-making body has recommended maintaining the EPF interest rate at 8.25% per annum for the financial year 2025–26. This rate, among the safest returns available, applies to the portion of your balance that remains untouched.

The Compliance Lens — procedural improvements and areas of clarity

| Area | Previous Approach | Current Approach |

| Withdrawal categories | 13 categories with complex conditions | 3 unified groups — easier to navigate |

| Employer share access | Restricted to retirement/disability | Fully accessible during unemployment |

| Final settlement timeline | 2 months of unemployment | 12 months of unemployment |

| Pension withdrawal timeline | 2 months of unemployment | 36 months of unemployment |

| Minimum balance protection | None — many exhausted full corpus | 25% preserved for 12 months |

Key considerations for employees

- Pension eligibility remains intact: Withdrawing your EPF balance does not affect your eligibility for pension at age 58, provided you have completed at least 10 years of EPS (Employee Pension Scheme) membership with consistent contributions. If you have less than 10 years of service, you can withdraw your accumulated EPS amount at any time during those 10 years.

- No impact on future employment: A partial withdrawal does not break your service continuity or reset your pension eligibility clock; a crucial protection for those who find new jobs within the 12-month window.

- Emergency access remains flexible: Even without unemployment, for genuine emergencies like medical treatment or higher education, you can withdraw from EPF without lengthy justification.

A final word of caution

While the new rules give you faster access to your hard-earned money, treat EPF as what it was designed for — retirement security. Dipping into it during unemployment is understandable and sometimes necessary. But wherever possible, keep the withdrawal amount limited and preserve the compounding power of that 8.25% interest for your later years.

Disclaimer

This content is for general informational purposes only and does not constitute legal, tax, or financial advice. EPFO rules and interpretations may vary by region and individual circumstances. Readers should consult qualified professionals for advice specific to their situation.