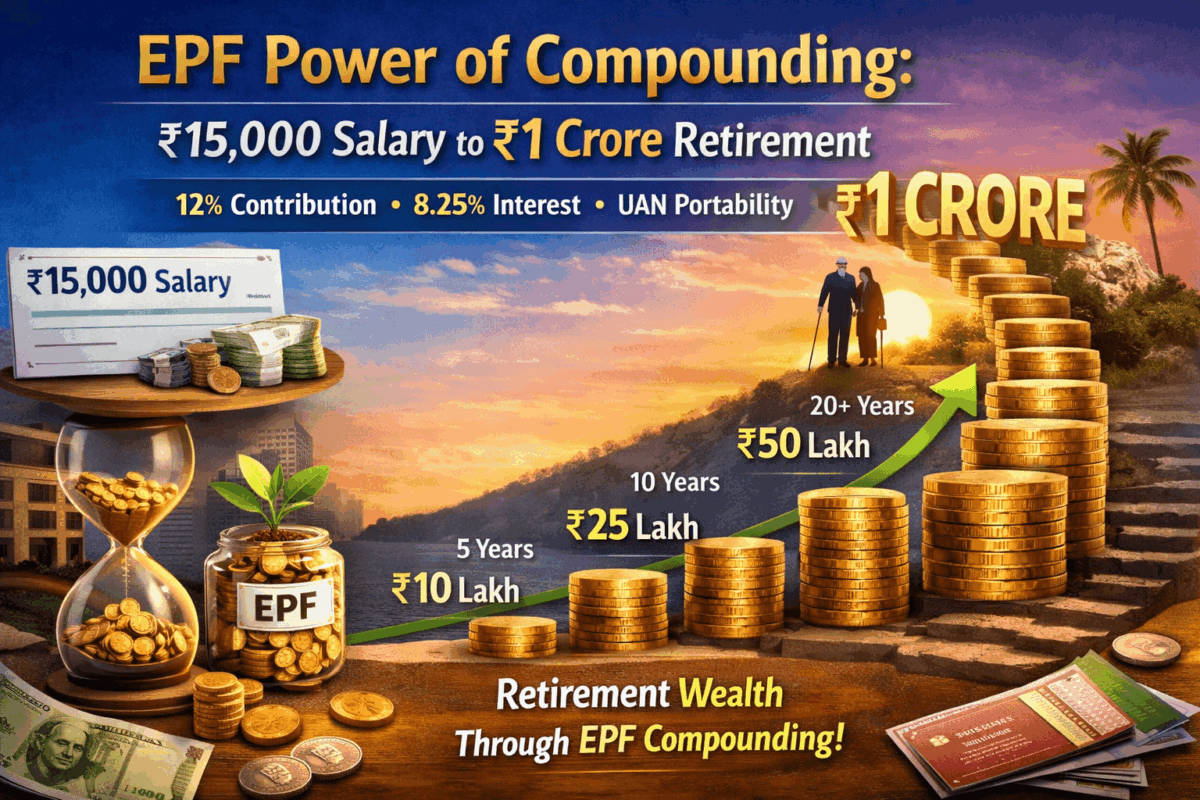

Financial independence is not limited to high earners. India’s Employees’ Provident Fund (EPF) demonstrates how disciplined saving and the principle of compounding can transform modest monthly contributions into a substantial retirement corpus. With a starting salary of ₹15,000, young professionals can realistically target savings exceeding ₹1 crore over a 30–35-year career.

In a Nutshell

By mandating contributions from both employees and employers, EPF ensures long-term wealth creation. The key lies in consistency, compounding, and resisting premature withdrawals.

The Breakdown

- The Math of 12%: Employees contribute 12% of basic pay plus dearness allowance (DA) to EPF. Employers match this, with 3.67% directed to EPF and 8.33% (capped at ₹1,250 per month) allocated to the Employees’ Pension Scheme (EPS).

- The Compounding Magic: EPF currently offers an annual interest rate of 8.25% (2025–26), compounded yearly. Over decades, this “snowball effect” multiplies savings, turning modest deposits into significant wealth.

- The Salary Hike Factor: With annual increments of 5–7%, contributions rise alongside paychecks, accelerating corpus growth.

- Discipline Over Decades: Avoiding non-essential withdrawals is critical. While EPFO permits advances for housing or emergencies, leaving funds untouched maximizes compounding power.

Compliance Lens

Legal and professional experts highlight several challenges:

- The ₹15,000 Ceiling Challenge: Employer contributions to EPS are capped at a ₹15,000 wage ceiling. Policy discussions in 2026 have suggested raising this to ₹25,000, which would enhance pension security.

- Taxation Thresholds: Under current tax rules, interest earned on employee contributions exceeding ₹2.5 lakh annually is taxable. High earners using Voluntary Provident Fund (VPF) must monitor this limit to avoid unexpected liabilities.

- UAN Portability: Ensuring seamless transfer of the Universal Account Number (UAN) during job changes is vital. Dormant accounts stop earning interest, slowing progress toward the ₹1 crore goal.

Legal Context

- EPF Act, 1952: Governs provident fund contributions and withdrawals.

- Employees’ Pension Scheme, 1995 (EPS-95): Provides pension benefits, subject to the wage ceiling.

- Income-tax Act, 2025: Introduces taxation thresholds for high-value PF contributions.

- Social Security Code, 2020: Consolidates retirement and social security provisions under a unified framework.

Outlook

The EPF system demonstrates how modest salaries, disciplined savings, and compounding can create substantial retirement wealth. Observers note that raising the EPS ceiling, improving UAN portability, and clarifying taxation rules will be key to strengthening retirement security for India’s workforce.

Disclaimer: This content is provided for informational purposes only and does not constitute legal, financial, or professional advice. The calculations mentioned are indicative based on specific assumptions regarding interest rates and salary hikes. Actual returns may vary based on EPFO policy changes, taxation, and individual employment history. Readers should consult with a qualified financial advisor or use the official EPFO calculator for personalized planning.