Total Visitors

Total Visitors  Online Users

Online Users  Today

Today  Yesterday

Yesterday

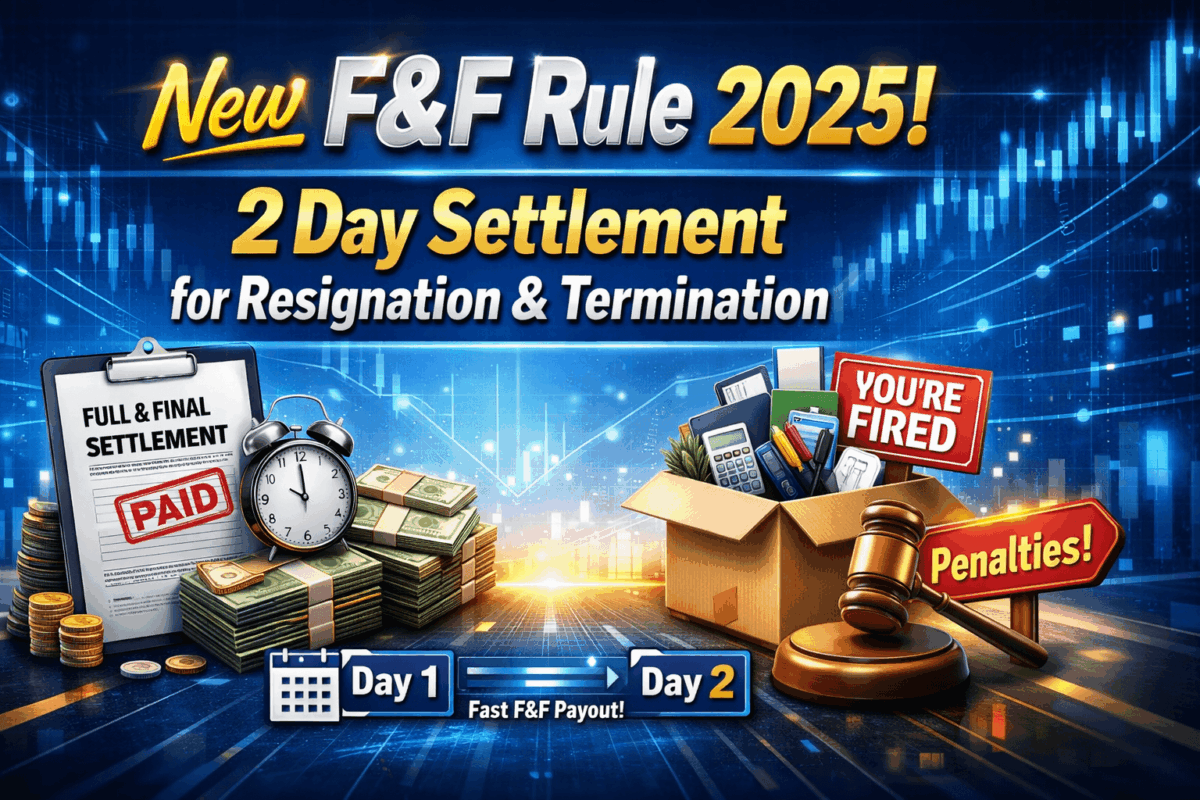

Full and Final (F&F) settlement has traditionally taken weeks in India; often 30, 45, or even 60 days. With the implementation of the Code on Wages, 2019, effective 21 November 2025, these timelines have been significantly shortened.

A common question is: does the two‑day rule apply only to terminations, or also to resignations? The answer, as the legal text makes clear, is both. This guide breaks down the law, the penalties, and the practical steps for both employees and employers.

1. The Legal Reality: Section 17(2) Explained

- Earlier regime (Payment of Wages Act, 1936):

- Termination: wages payable within 48 hours.

- Resignation: no statutory timeline; employers followed their own internal policies.

- New regime (Code on Wages, 2019 – Section 17(2)):

The Code explicitly states:

“Where an employee has been— (i) removed or dismissed from service; or (ii) retrenched or has resigned from service, or became unemployed due to closure of the establishment, the wages payable to him shall be paid within two working days of his removal, dismissal, retrenchment or, as the case may be, his resignation.”

The law removes the distinction between voluntary and involuntary exits. The two‑day clock starts from the Last Working Day (LWD).

2. What Is “Wages” Under the Code? (Section 2(y))

Understanding which payments are covered by the two‑day timeline requires knowing how the Code defines “wages.” Under Section 2(y) of the Code, “wages” means all remuneration capable of being expressed in money, and specifically includes:

- Basic Pay

- Dearness Allowance (DA)

- Retaining Allowance

The Code also introduces a “50% rule” for determining what constitutes wages. If the total of payments made to an employee that are excluded from the definition of wages (for example, HRA, conveyance allowance, overtime allowance, employer’s PF contribution, etc.) exceeds 50% of the total remuneration, then the excess amount shall be deemed to be part of “wages”.

3. Included vs. Excluded Payments

| Included (Must be paid within 2 days) | Excluded (Governed by separate statutes) |

| Pro‑rata salary for days worked in the final month | Gratuity — governed by the Payment of Gratuity Act / Social Security Code (typically 30 days) |

| Leave encashment for earned leave (included within the definition of wages under Section 2(y)) | EPF — governed by EPFO (settlement usually occurs after the employer files the required returns) |

| Statutory bonus due for the period worked (included as wages under Section 2(y) read with bonus provisions) | Employer’s contribution towards PF / pension |

| Fixed allowances forming part of “wages” (i.e., HRA, conveyance, and other allowances that exceed the 50% cap as per Section 2(y)) | Ex-gratia payments, retrenchment compensation, and other retirement benefits |

| HRA, conveyance allowance, travelling concession, overtime allowance, commission |

While the two‑day rule covers the “wage” components, the full F&F settlement may still include gratuity and EPF payments on their respective statutory timelines.

4. The Consequences of Delay (Section 54)

The Code on Wages sets out clear penalties for non‑compliance in Section 54. A delay in paying the F&F dues amounts to a contravention of Section 17, which falls under Section 54(1)(c).

| Stage of Violation | Applicable Clause | Penalty under Section 54 of the Code on Wages, 2019 |

| First Offence | Section 54(1)(c) | The employer shall be punishable with a fine which may extend to twenty thousand rupees. |

| Repeat Offence | Section 54(1)(d) | If the same contravention occurs again within five years, the penalty is imprisonment which may extend to one month or a fine up to forty thousand rupees, or both. |

The Role of the Inspector‑cum‑Facilitator

The Code also provides a key safeguard before prosecution. As per Section 54(3), before initiating legal action for a first‑time contravention, the Inspector‑cum‑Facilitator is required to give the employer a written direction to comply. Prosecution will not proceed if the employer complies within the period specified. However, this safeguard does not apply to repeat offences within five years.

5. The Claims Process: How Employees Can Enforce Their Rights

The Code on Wages (Section 45) establishes a dedicated mechanism for employees to recover unpaid or delayed wages.

| Provision | Details |

| Who can file a claim? | The employee, a registered trade union of which the employee is a member, or the Inspector‑cum‑Facilitator |

| Multiple employees | A single application can be filed on behalf of any number of employees in an establishment |

| Limitation period | Within 3 years from the date the claim arises; the Authority may condone delay upon sufficient cause |

| What can the Authority order? | The claim amount plus compensation up to ten times the claim amount |

| Decision timeline | The Authority shall endeavour to decide the claim within 3 months |

| Appointment of Authority | One or more authorities, not below the rank of a Gazetted Officer, appointed by the appropriate Government |

| Powers of the Authority | Has all the powers of a civil court for taking evidence, enforcing attendance of witnesses, and compelling production of documents |

| What if the employer still doesn’t pay? | The Authority issues a recovery certificate to the Collector or District Magistrate, who recovers the amount as arrears of land revenue |

| Appeal | Within 90 days to the appellate authority appointed by the appropriate Government; the appellate authority shall endeavour to dispose of the appeal within 3 months |

6. Permissible Deductions from Wages (Section 18)

The Code on Wages also limits what an employer can deduct from an employee’s wages. Under Section 18, employers may only make deductions for specified purposes, such as:

- Fines imposed on the employee

- Absence from duty

- Damage to or loss of goods entrusted to the employee

- Recovery of advances, loans, or overpayments

- Income tax and other statutory deductions

- Contributions to provident fund, trade union fees, etc.

Critically, the total deductions from an employee’s wages in any wage period shall not exceed 50% of the total wages payable. This cap ensures that employees receive at least half of their earned wages in every wage period.

7. Practical Considerations for Employers

Compliance with the two‑day rule requires operational changes:

- Digitize clearances: Replace paper‑based “No Dues” forms with real‑time portals for exit approvals.

- Pre‑emptive processing: Initiate clearance workflows during the notice period, before the employee’s LWD.

- Automate payroll: Ensure the system can calculate pro‑rata dues instantly upon exit.

- Set up a Section 45‑ready process: Be prepared to respond to claims within the statutory framework, including producing evidence of payments, deductions, and compliance.

Employees may be asked to return company assets (laptops, ID cards, etc.) or complete exit formalities before their LWD to enable timely settlement — a reasonable practice that facilitates compliance.

8. Final Thoughts

The two‑day F&F rule is a landmark reform. It ensures resignation is treated with the same urgency as termination, protecting employee liquidity and ending the era of prolonged settlement delays. Employers who fail to adapt risk fines, recovery certificates, and, for repeat offences, even imprisonment. Employees, for their part, are empowered with a robust Section 45 claims mechanism backed by recovery as land revenue arrears and appeal rights up to the appellate authority.

- For Employers: Audit exit workflows, digitize clearance processes, and understand the 50% deduction cap under Section 18.

- For Employees: Know your rights under Section 17(2) and Section 45, cooperate with exit procedures to enable smooth compliance, and file claims within the three‑year limitation period if needed.

Disclaimer: This article is for general informational and educational purposes only and does not constitute legal advice. Laws may vary by state. Readers should consult a qualified legal professional or authorised labour law consultant for specific guidance on F&F settlements.