Total Visitors

Total Visitors  Online Users

Online Users  Today

Today  Yesterday

Yesterday

Why This Matters Today

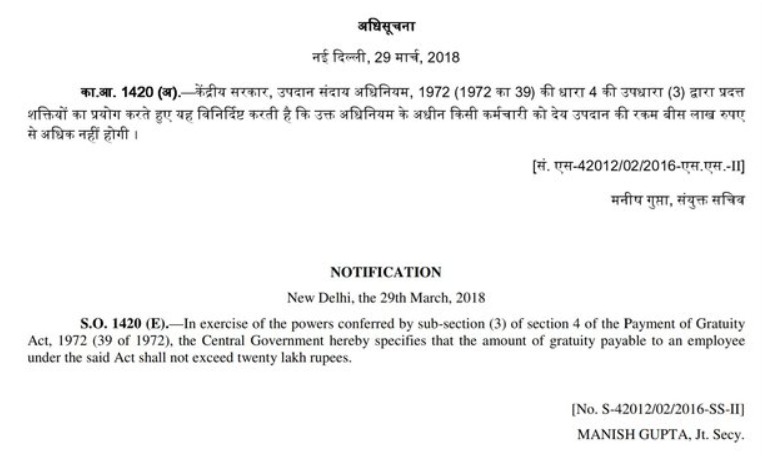

Gratuity remains one of the most sensitive statutory payouts in India. The ceiling of ₹20 lakh under the Payment of Gratuity Act, 1972 (via Notification S.O. 1420(E), dated 29 March 2018) continues under the Code on Social Security, 2020. For central government employees, the cap is ₹25 lakh.

The critical point: there is no bar on employers paying more than the statutory ceiling. However, any excess loses its legal character as “gratuity” and is treated as ex‑gratia, fully taxable under Section 10(10) of the Income Tax Act. HR leaders must therefore distinguish between statutory liability and voluntary generosity.

Gratuity Ceiling Across Categories

| Category | Statutory Ceiling | Notes |

| Private sector employees (Payment of Gratuity Act, 1972) | ₹20 lakh | As per the 2018 notification, gratuity payable under the Act cannot exceed ₹20 lakh. Employers may pay more, but excess is taxable. |

| Private sector employees (Code on Social Security, 2020) | ₹20 lakh | The Code consolidates gratuity provisions and retains the ₹20 lakh cap. Fixed-term employees become eligible after 1 year of service. |

| Central Government employees | ₹25 lakh | The ceiling was raised for government employees; exemption under Income Tax Act also applies up to ₹25 lakh. |

| State Government employees | Varies | Most states follow the ₹20 lakh cap, unless a specific state notification provides otherwise. |

| Employer voluntary payments | Beyond ₹20 lakh | Employers can pay more than the statutory ceiling, but only ₹20 lakh (₹25 lakh for central govt) is exempt from tax. Excess is taxable in the employee’s hands. |

Legacy vs. Code Regime: What Changed

| Provision | Legacy Framework | Code Framework (2026) |

| Gratuity Ceiling | ₹20 lakh (2018 notification) | ₹20 lakh retained under Code on Social Security |

| Eligibility | 5 years continuous service | Fixed-term employees eligible after 1 year |

| PF Ceiling | ₹15,000/month | No notified change |

| Bonus Ceiling | Eligibility ₹21,000; calc ₹7,000/min wage | Retained under Code on Wages |

| ESI Ceiling | ₹21,000/month | Retained under Code on Social Security |

| Exit Settlements | Often delayed | Mandatory within 2 days (48‑Hour Exit Rule) |

Compliance Checklist for HR Directors [FREE]

- Gratuity: Cap liability at ₹20 lakh. Record any excess as ex‑gratia.

- PF: Ensure wage ceiling compliance at ₹15,000/month.

- Bonus: Apply eligibility ceiling of ₹21,000/month and calculation ceiling of ₹7,000/minimum wage.

- ESI: Cover employees earning up to ₹21,000/month.

- Wage Structuring: Apply the 50% wage rule (Basic + DA ≥ 50% of gross).

- Exit Settlements: Complete full and final within 2 days.

- Fixed-Term Employees: Track gratuity eligibility after 1 year.

- Gig/Platform Workers: Ensure aggregator contributions are mapped.

Operational Challenges and Risks

- Audit risk: Misclassifying payments beyond ₹20 lakh as “gratuity” can trigger objections.

- Payroll friction: Systems must distinguish gratuity vs. ex‑gratia.

- Tax exposure: Employees receiving more than ₹20 lakh face tax liability on the excess.

- Strategic HR alignment: Employers may use ex‑gratia payments for retention or goodwill, but must disclose them separately.

Disclaimer: This content is for educational and informational purposes only. It is based on Central and State notifications available as of July 2026. It does not constitute formal legal advice. Readers should consult qualified counsel before making compliance decisions.