Total Visitors

Total Visitors  Online Users

Online Users  Today

Today  Yesterday

Yesterday

For mobility platforms, quick‑commerce aggregators, and tech‑driven fleet operators in India, risk management is a regular part of doing business. As the Code on Social Security, 2020 along with the Social Security (Central) Rules, 2026 move into full effect, corporate legal clinics are witnessing an influx of complex, multi‑jurisdictional compliance inquiries.

With the government enforcing a strict data‑synchronisation deadline for digital aggregators to integrate their fleet ledgers with the central e‑Shram portal, a highly practical cross‑platform dispute has emerged.

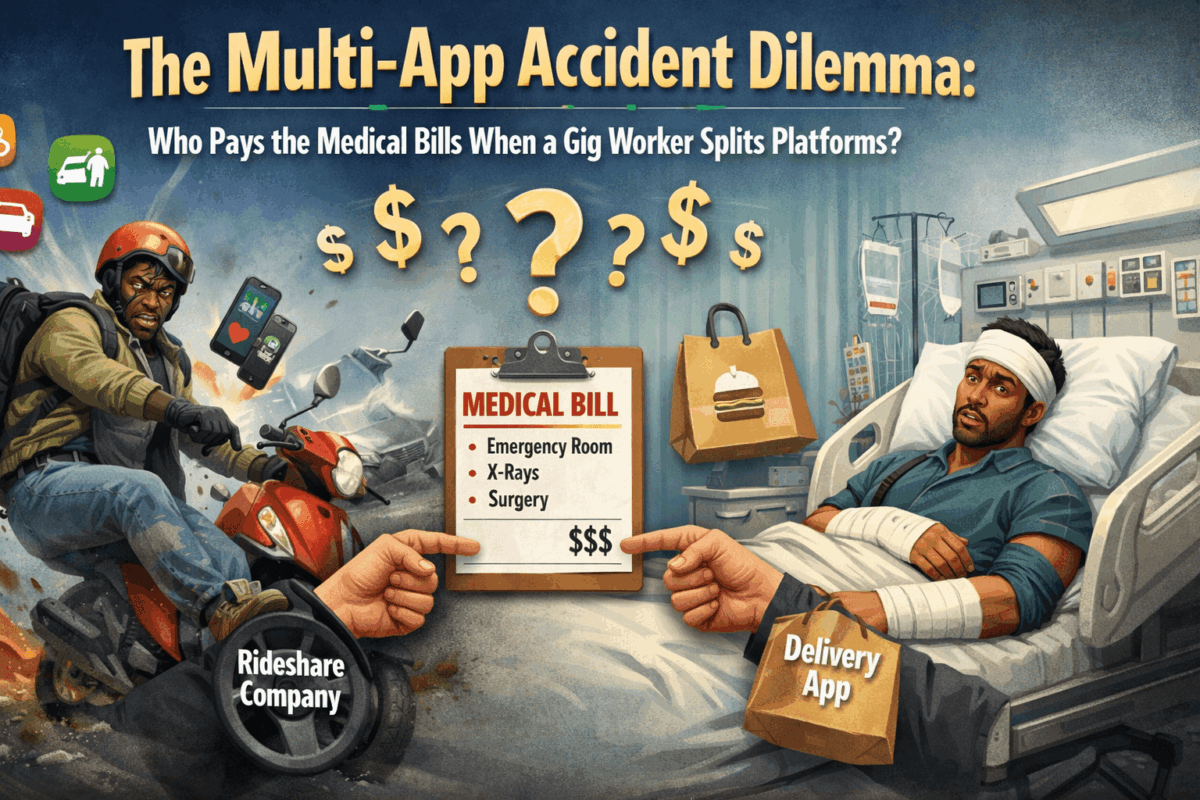

Consider this real‑world scenario frequently raised by fleet operations managers:

A ride‑hailing driver operates on the Ola platform for 80 days in a financial year, then switches over to Uber for the next 30 days. On his 30th day with Uber, he meets with a severe accident while actively executing a ride. Which aggregator‘s social security fund is liable to clear his medical bills? Ola? Uber? Both? Or neither?

If your HR operations or legal departments are relying on generic, pre‑code contractor guidelines to resolve this claim, your enterprise is exposed to significant structural risks. Let’s look past the user‑interface screens to analyse how the law parses overlapping timelines, intersects with concurrent transport regulations, and establishes liability.

The Executive Context: Solving the 90/120‑Day Statutory Puzzle

To determine liability accurately, management must first look at the newly finalised eligibility filters built into the central social security rules. The Social Security (Central) Rules, 2026 split social security access using two distinct temporal baselines:

- The Single‑Platform Gateway: A gig worker requires a minimum of 90 active engagement days with a single aggregator within a financial year to unlock state‑notified welfare scheme benefits from the central fund.

- The Multi‑Platform Gateway: If a worker distributes their hours across competing digital networks, they require a minimum of 120 cumulative engagement days across all platforms within the same financial year.

Under the “income earned” rule, a worker is considered “engaged” for one day if they earn income, regardless of the amount, on that calendar day. Working across multiple aggregators on the same day counts as multiple engagement days.

Let‘s apply the strict math of the rules to our driver’s timeline:

80 Days (Ola) + 30 Days (Uber) = 110 Cumulative Days

Because the driver‘s total across all applications equals 110 days, they fall exactly 10 days short of the mandatory 120‑day multi‑platform threshold. Furthermore, they have not reached the 90‑day single‑platform baseline on either application individually.

The Statutory Verdict for the Central Fund: Under the strict rules of the Code on Social Security, neither Ola nor Uber‘s contributions to the Central Gig Workers’ Social Security Fund can be drawn upon to fund this specific medical claim. Statutorily, the worker has not yet entered the central welfare eligibility zone.

Note: The National Social Security Board for Gig and Platform Workers chaired by the Union Labour Secretary and including representatives from the Ministry of Finance, Ministry of Electronics & IT, NITI Aayog, five state governments, and worker/employer organisations oversees the administration of this central fund.

The Concurrent Framework Check: The MoRTH Insurance Mandate

Does this mean the platform escapes all financial exposure for the accident? Absolutely not.

While the central social security fund remains locked due to the 120‑day threshold gap, a parallel, concurrent regulatory framework applies. Because transport and labour are governed under the Concurrent List of the Indian Constitution, aggregators must look directly at the Motor Vehicle Aggregator Guidelines, 2020 issued by the Ministry of Road Transport and Highways (MoRTH), alongside state‑specific adoptions.

Under the MoRTH Guidelines, the financial liability shifts from a centralised state fund to direct, mandatory corporate insurance:

- The Insurance Mandate: Every aggregator is legally required to provide comprehensive Health Insurance (minimum ₹5 lakh) and Term Insurance (minimum ₹10 lakh) for every driver registered on their platform.

- Annual Escalation: The coverage amount increases by 5% each year from the base year 2020‑21.

- The Active App Principle: Liability for an on‑the‑job accident attaches strictly to the platform on which the ride was booked and executed during active duty hours.

The Operational Verdict: Because the accident occurred while the driver was actively fulfilling a trip for Uber, Uber‘s mandatory corporate group health insurance policy is 100% liable for the medical bills from day one. Ola has zero liability for this accident, as the worker was not engaged on their digital network when the incident occurred.

Industry Note: Aggregators have raised concerns about duplication of costs under the central fund and the existing MoRTH insurance mandate. However, both obligations remain legally distinct and enforceable.

Dual‑Regime Analysis: Central Fund vs. MoRTH Insurance

| Compliance Vector | Central Social Security Fund | MoRTH Aggregator Guidelines, 2020 |

| Governing Authority | Ministry of Labour & Employment | Ministry of Road Transport and Highways |

| Eligibility Trigger | 90 days (single aggregator) or 120 days (multiple aggregators) | From the moment a driver is registered on the platform (no minimum engagement) |

| Medical Coverage | Subject to scheme notification | ₹5 lakh health insurance + ₹10 lakh term insurance, escalating 5% annually |

| Liability Basis | Pro‑rated via aggregator turnover contribution | Direct corporate insurance policy |

| Penalty for Non‑Compliance | 12% annual interest on delayed contributions | Potential suspension of transport license |

2026 Core Impact Filters for Corporate Restructuring

When executing an internal audit of your logistics or delivery operations this year, you must evaluate how gig worker protection tracking interacts with broader compliance filters:

The Reclassification Guardrail

Traditional corporate payrolls must satisfy the strict 50% Wage Rule (basic salary ≥50% of CTC) and the 48‑Hour Exit Rule (full settlement within 2 working days). Because gig workers operate under flexible, transaction‑based fees rather than regular salary components, they remain exempt from these allocation rules. However, to maintain this protection, platforms must avoid traditional payroll language in their partner agreements, as doing so can prompt tribunals to reclassify gig fleets as permanent staff; as seen in the Karnataka High Court ruling that held Ola liable under the PoSH Act, treating a driver‑subscriber as an “employee”.

The Third‑Party Fleet Loophole Barrier

The definition of “aggregator” under the Code includes any entity that coordinates with one or more aggregators for providing services, extending liability to associate companies, subsidiaries, and third‑party logistics intermediaries. If a platform attempts to route its fleet through local sub‑contracted vendors, the primary aggregator remains directly liable under the code to ensure that every driver is mapped to a verified Universal Account Number (UAN) and covered by the day‑one insurance mandate.

The State‑Level Welfare Fee Layer

States like Karnataka, Rajasthan, and Telangana have enacted or proposed their own welfare regimes. Karnataka imposes a 1‑5% per transaction welfare fee deducted from worker payouts, adding compliance complexity atop the central framework.

Core Compliance Checklist for Platform Executives – FREE

To protect your organisation against interest penalties, class‑action disputes, and transport license suspensions, your operations and risk management teams should satisfy this checklist:

- Audit Day‑One Insurance Activations: Verify that your insurance providers automatically activate the mandatory ₹5 lakh health and ₹10 lakh term covers the moment a new partner completes onboarding, without waiting for the 90‑day e‑Shram milestone. Ensure the coverage increases by 5% annually from the 2020‑21 base year.

- Configure “Active Ride” Data Logs: Maintain clear, timestamped records of when a driver logs in, accepts a trip, and logs off. If an accident occurs, your system must provide instantaneous proof of whether the partner was on an active delivery or ride path.

- Automate UAN Verification During Onboarding: Update your digital onboarding sequence to ensure that all delivery partners and drivers link their active profiles to a verified e‑Shram Universal Account Number (UAN) using Aadhaar‑seeded authentication.

- Implement Real‑Time Reporting: Under the Social Security (Central) Rules, 2026, every aggregator engaging a new gig worker must register them on the central portal in real time and report their exit. Non‑compliance can trigger automated flags in unified electronic returns.

- Maintain Turnover Contribution Reserves: Ensure your corporate treasury sets aside the mandatory 1‑2% turnover levy for the Central Social Security Fund, capped strictly at 5% of total worker payouts, independent of private insurance premiums.

- Track State‑Level Notifications: Monitor emerging gig worker welfare legislation in Karnataka, Rajasthan, Telangana, and other states to ensure dual compliance with central and state frameworks.

Financial and Operational Risk Analysis

The financial and operational fallout of mismanaging fleet insurance or failing to maintain accurate data syncs can quickly impact your balance sheet:

| Risk Category | Operational Implication | Legal & Financial Fallout |

| Delayed Contribution | Failing to calculate or deposit turnover levy within timelines. | 12% annual interest penalty (1% per month) on delayed amount. |

| Uninsured Fleet Accident | Driver lacks active ₹5 lakh health cover at time of accident. | Transport Authority may suspend aggregator license; direct corporate liability for all medical claims. |

| Multi‑App Eligibility Gap | Worker falls short of 90/120‑day threshold for central fund. | Worker cannot access central fund, but MoRTH insurance remains primary liability source. |

| Third‑Party Vendor Non‑Compliance | Sub‑contracted fleet operator fails to maintain proper insurance records. | Parent aggregator held directly liable for all indirect fleet compliance breaches. |

| Real‑Time Reporting Failure | New worker registrations not reported to e‑Shram portal in real time. | Automated flags in unified digital returns, leading to targeted labour inspections. |

Furthermore, if an aggregator experiences a high frequency of un‑synchronised data or fails to process active‑trip insurance claims promptly, it can trigger automated exceptions in the government‘s unified electronic returns. This can lead to unexpected labour inspections and create significant administrative hurdles for your leadership team during standard corporate compliance audits.

Conclusion

The multi‑app accident dilemma reveals a critical structural feature of India‘s new gig worker protection framework: two parallel, non‑overlapping liability tracks.

Track 1 – Central Social Security Fund: Governed by the 90/120‑day eligibility rule. Workers who split their time across platforms may fall short of the cumulative threshold, making them ineligible to draw benefits from the central fund – even though their aggregators have contributed 1‑2% of turnover.

Track 2 – MoRTH Mandatory Insurance: Operates from day one of platform registration, independent of engagement thresholds. Provides ₹5 lakh health and ₹10 lakh term insurance, with liability attaching to the platform on which the active ride was booked.

The practical answer to our opening scenario is clear: Uber pays. The central fund’s 90/120‑day rule does not let the platform off the hook; the MoRTH Guidelines create a separate, enforceable obligation that activates immediately upon onboarding.

Smart aggregators will:

- Audit day‑one insurance activation for every registered driver,

- Maintain timestamped active ride logs to resolve liability disputes,

- Implement real‑time e‑Shram reporting for new worker appointments and exits,

- Monitor state‑level welfare fee notifications across Karnataka, Rajasthan, Telangana, and other states, and

- Ensure third‑party fleet vendors are contractually bound to maintain identical insurance and data reporting standards.

Disclaimer: This publication is provided for general informational and educational purposes only and does not constitute legal advice. The information contained herein may not reflect the most current legal developments and is not guaranteed to be complete, accurate, or up‑to‑date. Nothing in this publication creates a lawyer‑client relationship between the reader and the author or publisher. Laws, regulations, and judicial interpretations vary by jurisdiction and may change over time. Readers should not act or refrain from acting on the basis of any information contained in this publication without first seeking independent legal counsel from a qualified lawyer licensed to practice in the relevant jurisdiction. The author and publisher expressly disclaim all liability in respect of any actions taken or not taken based on any or all of the contents of this publication. Case citations and statutory references are provided for illustrative purposes only and do not constitute a guarantee of any particular outcome. Always consult a qualified legal professional for advice tailored to your specific circumstances.