Total Visitors

Total Visitors  Online Users

Online Users  Today

Today  Yesterday

Yesterday

For corporate leaders, CHROs, and legal counsels navigating India‘s updated regulatory landscape, the Industrial Relations (IR) Code, 2020 stands as a landmark structural reform. A primary talking point of this framework is the modification of the statutory threshold under Chapter X. Under the legacy regime, establishments with 100 or more workers required prior approval from the appropriate government authority before executing a layoff, retrenchment, or closure. The active code regime raises this threshold to 300 workers, designed to foster ease of doing business and eliminate rigid operational bottlenecks for mid-sized enterprises.

However, this policy shift has sparked a major compliance misconception: the belief that an enterprise employing less than 300 individuals (such as a firm with exactly 299 workers) can execute layoffs or terminations “with no questions asked” simply by serving a standard notice and minimal compensation.

To assume that a 299‑employee operation operates in a regulatory vacuum is an expensive mistake. The active code regime provides flexibility by removing the need for prior government permission, but it does not remove the employee’s fundamental legal protections. Layoffs and permanent terminations (retrenchments) remain bound by clear statutory criteria, strict timeline rules, and established principles of natural justice.

Important Clarification on the 300‑Worker Threshold

The 300-worker threshold under Chapter X of the IR Code, 2020 applies only to the requirement of obtaining prior government permission before a layoff, retrenchment, or closure. The substantive financial obligations including 15 days‘ wages per year as retrenchment compensation and the Worker Re‑skilling Fund contribution apply to all retrenchments, regardless of the establishment’s headcount, provided the worker has completed at least one year of continuous service. In other words:

- Headcount determines if you need permission.

- Headcount does NOT change what you must pay the worker.

The Legacy vs. New Rules Comparison

To understand the boundaries of an exempt establishment, we must distinguish between two legally distinct corporate actions that are often conflated:

- Lay‑off: A temporary inability to provide work due to reasons like power shortages, raw material deficits, or natural calamities, where the employment relationship continues.

- Retrenchment: The permanent termination of a worker’s services for economic, structural, or redundant reasons (excluding disciplinary dismissals).

The following comparative table illustrates how protections scale across thresholds under both the legacy and active frameworks.

| Compliance Vector | The Legacy Regime (Industrial Disputes Act, 1947) | The Active Code Regime (IR Code, 2020 & Central Rules, 2026) |

| Prior Government Permission Threshold | Mandatory for industrial establishments with 100 or more workers (Chapter V‑B). | Mandatory only for factories, mines, and plantations with 300 or more workers (Chapter X). |

| Temporary Lay‑off Compensation (50–299 Workers in Factories/Mines/Plantations) | 50% of basic wages + DA for up to 45 days (Section 25‑C). No prior permission needed. | 50% of basic wages + DA + Retaining Allowance under Section 67. No prior permission needed. |

| Permanent Retrenchment Payout (for all eligible workers, regardless of headcount) | 1 month‘s notice (or wages in lieu) + 15 days’ average pay per year of continuous service. | 1 month‘s notice (or wages in lieu) + 15 days‘ last drawn wages per year of continuous service + mandatory Worker Re‑skilling Fund contribution (Section 70 read with Section 83). |

| Full & Final Settlement Timeline | Variable across state‑specific Shops & Establishments Acts (typically 7 to 30 days). | The 48‑Hour Exit Rule under Section 17(2), Code on Wages, 2019 – wages payable within 2 working days of separation. |

| Worker Redressal Route | Long conciliation bottlenecks; subject to state government reference orders. | 45‑Day Conciliation window, followed by direct Industrial Tribunal access under Section 91. |

The Legal Reality: Why the 299th Employee Has Substantial Recourse

If a company with 299 workers attempts to permanently terminate or temporarily lay off an employee arbitrarily, the action can be legally challenged on several grounds.

1. The Distinction Between “Permission” and “Compensation”

The 300‑worker threshold removes the need for prior government permission before a layoff, retrenchment, or closure. However, it does not remove the employer‘s obligation to pay statutory compensation. The substantive rules that protect workers including severance pay, notice periods, and the Worker Re‑skilling Fund apply to all retrenchments, irrespective of headcount.

2. The “Last Come, First Go” Rule and Re‑employment Rights (Sections 71 & 72)

If the employer intends a permanent separation (retrenchment) for the 299th worker, they must strictly satisfy the statutory mandates of Section 70 of the IR Code. The business cannot terminate “with no questions asked.” The employer must demonstrate:

- The “Last Come, First Go” Rule (Section 71): The employer must systematically retrench the last person hired in that category, unless there are fully documented, objective reasons to deviate.

- The Re‑employment Right (Section 72): If the company hires for the same role within one year, the retrenched 299th employee must be offered the position first.

3. The Structural Wage Impact and the 48‑Hour Exit Rule

The financial math behind termination compensation is no longer open to creative accounting. Under the 50% Wage Rule across the Codes, an employee’s “wages” for the calculation of the 15‑day retrenchment compensation must be calculated based on a base that constitutes at least 50% of their total remuneration structure (Section 2(y) of the Code on Wages, 2019).

Furthermore, under the 48‑Hour Exit Rule found in Section 17(2) of the Code on Wages, 2019, all wages payable (Basic Pay + DA + Retaining Allowance) must be paid within two working days of separation. Gratuity and retrenchment compensation follow their own statutory timelines, but best practice strongly favours prompt settlement to avoid adverse judicial inference.

Important: Employers are also required to contribute 15 days’ last drawn wages per retrenched worker to the Worker Re‑skilling Fund under Section 83 of the IR Code, 2020. This contribution must be made within ten days at the time of retrenchment and is in addition to retrenchment compensation paid directly to the worker. The government then credits the amount to the worker‘s account within 45 days.

Core Compliance Checklist for HR and Management – FREE

To prevent transitional friction and limit corporate exposure when resizing a team in an establishment with less than 300 workers, ensure your HR teams follow this checklist:

- Verify Worker Classification: Confirm if the individual falls under the expanded definition of “worker” under Section 2(zr) of the IR Code. Supervisory employees earning up to ₹18,000 per month are now classified as workers and protected under retrenchment clauses.

- Understand the 300‑Worker Threshold: The only change is the removal of prior government permission. All financial obligations (retrenchment compensation, notice pay, Reskilling Fund contribution) remain fully applicable. Do not assume the 300‑worker exemption allows you to skip statutory payouts.

- Audit the 50% Wage Structure: Recalculate your severance liabilities. Ensure that the “wages” baseline for compensation calculations is accurate; allowances cannot exceed 50% of total CTC, and any excess must be added back to the wage base.

- Fund the Worker Re‑skilling Fund: Under Section 83, for every worker retrenched, the employer must pay an additional sum equivalent to 15 days‘ last drawn wages into a government‑managed Reskilling Fund within the prescribed timeline (typically 10 days). This is an absolute corporate liability over and above the severance paid directly to the employee.

- Document the Business Case: Maintain clean, objective documentation for the downsizing (e.g., technology redundancy, structural shifts, proven market slowdowns) to defend against claims of targeted or colourable exercise of power before an Industrial Tribunal.

- Enforce 48‑Hour Wage Payout: Ensure payroll and finance can process accurate wage calculations, including any wages due, within the strict 2‑working‑day legal window under Section 17(2), Code on Wages, 2019.

- Adopt Model Standing Orders Baseline: Even without certified Standing Orders, the Central or State Model Standing Orders apply as a default statutory floor of service conditions. Ensure your policies align with these standards.

Financial and Operational Risk Analysis

Viewing the 300‑employee exemption as a license for unrestricted downsizing can lead to severe operational challenges:

| Risk Category | Operational Implication | Legal & Financial Fallout |

| Misunderstanding the 300‑worker threshold | Assuming that the 300‑worker exemption eliminates all statutory obligations. | The employer may fail to pay retrenchment compensation or the Reskilling Fund contribution, exposing them to significant statutory penalties and employee claims. |

| Delayed Contribution | Failing to deposit the Worker Re‑skilling Fund contribution within the prescribed timeline (typically 10 days). | Statutory interest penalties may apply; potential fines for non‑compliance. |

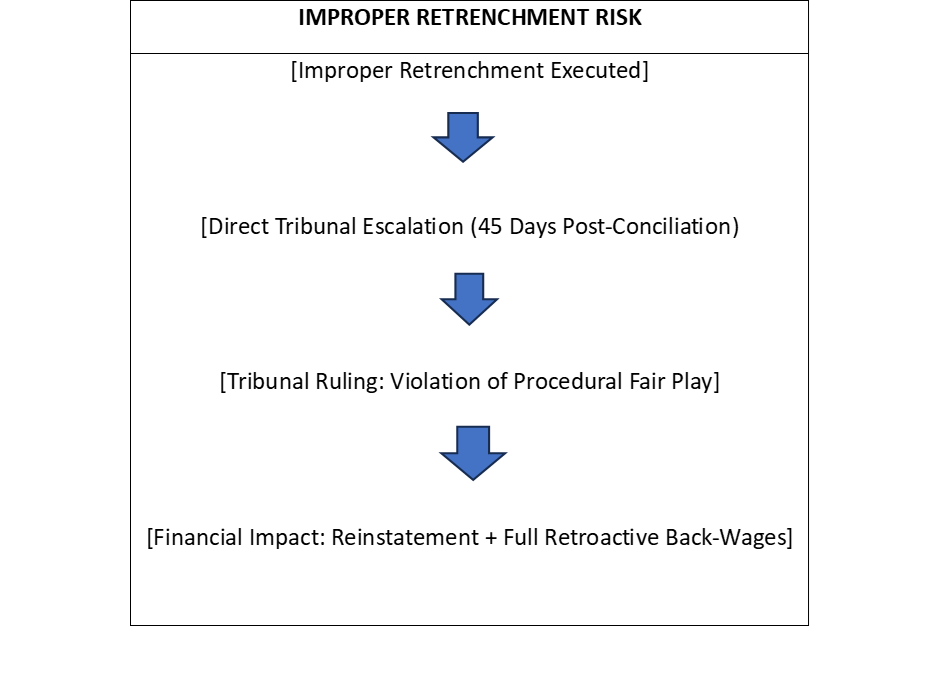

| Procedural Violation | Retrenching a worker without following the “last come, first go” rule or providing required notice. | Industrial Tribunal may declare termination void; reinstatement with full back‑wages. |

| Unfair Labour Practice | Arbitrary termination without documented business justification or domestic inquiry. | Additional penalties under Second Schedule, IR Code, 2020; reputational damage. |

| 48‑Hour Wage Default | Failing to settle wages within 2 working days of separation. | Interest penalties; potential legal challenge; adverse judicial inference. |

| 50% Wage Miscalculation | Under‑calculating retrenchment compensation by distorting wage structures. | Statutory penalties under the Code on Wages, 2019; exposure to employee claims. |

Penalty Framework Under the IR Code, 2020

Different contraventions carry different penalty ranges:

| Violation | Applicable Section | First Offence Penalty | Subsequent Offence Penalty |

| Contravening closure provisions (Section 78/79/80) | Section 86(1) | ₹1,00,000 – ₹10,00,000 | ₹5,00,000 – ₹20,00,000 + imprisonment up to 6 months |

| Contravening retrenchment provisions (Section 70) | Section 86(3) | ₹50,000 – ₹2,00,000 | ₹1,00,000 – ₹5,00,000 + imprisonment up to 6 months |

| Unfair labour practice (Second Schedule) | Section 86(5) | ₹10,000 – ₹2,00,000 | ₹50,000 – ₹5,00,000 + imprisonment up to 3 months |

Additionally, non‑compliance with retrenchment compensation frameworks or failure to contribute to the Reskilling Fund invites significant structural fines, creating unnecessary financial and reputational exposure for growing brands.

Disclaimer: This publication is intended solely for educational, informational, and general corporate awareness purposes. The insights and analyses contained herein are formulated based on the Central and State subordinate rules notified by the Government of India as available up to the current date of 2026. This content does not constitute, nor is it intended to substitute for, formal legal advice, structural statutory audits, or professional legal counsel. Organizations are strongly advised to retain qualified labour law practitioners to evaluate state-specific rules and unique organizational scenarios before enacting structural workforce adjustments.